IVA debt advice can help you find a suitable solution if you owe substantial unsecured debts to multiple creditors and are struggling to afford repayments.

Top 5 Best IVA Debt Companies in UK 2024

If you’re starting to feel overwhelmed by mounting debt, you likely have a sense that there’s “no way out.” Many Brits find themselves in this very position, and this is when gathering IVA debt advice can go a long way to helping you gather the advice you need to achieve a debt-free, financially balanced lifestyle. Seeking IVA debt help can be the first step you take towards regaining control of your financial situation. Remember that IVA debt management isn’t always the best solution for everyone. Because of this, it’s a great idea to get the professional advice of a debt IVA specialist who can advise you on your circumstances.

If you want to know what is an IVA debt plan or if you’d like to compare a debt management plan vs IVA, you’ve taken a step in the right direction. Below, we will explain what’s an IVA debt plan, how IVA debt consolidation works, and offer additional advice to help you get your finances back on track.

ADVERTISEMENT

Top Companies Offering IVA Debt Advice in the UK

- Debt Nurse: Leading Platform for Gathering IVA Debt Help and Guidance

- Help My Debts Pro: Top Option for Connecting with Debt IVA Advisors in the UK

- 123 Debt Fix: Good Starting Point for People Interested in an IVA Debt Write Off

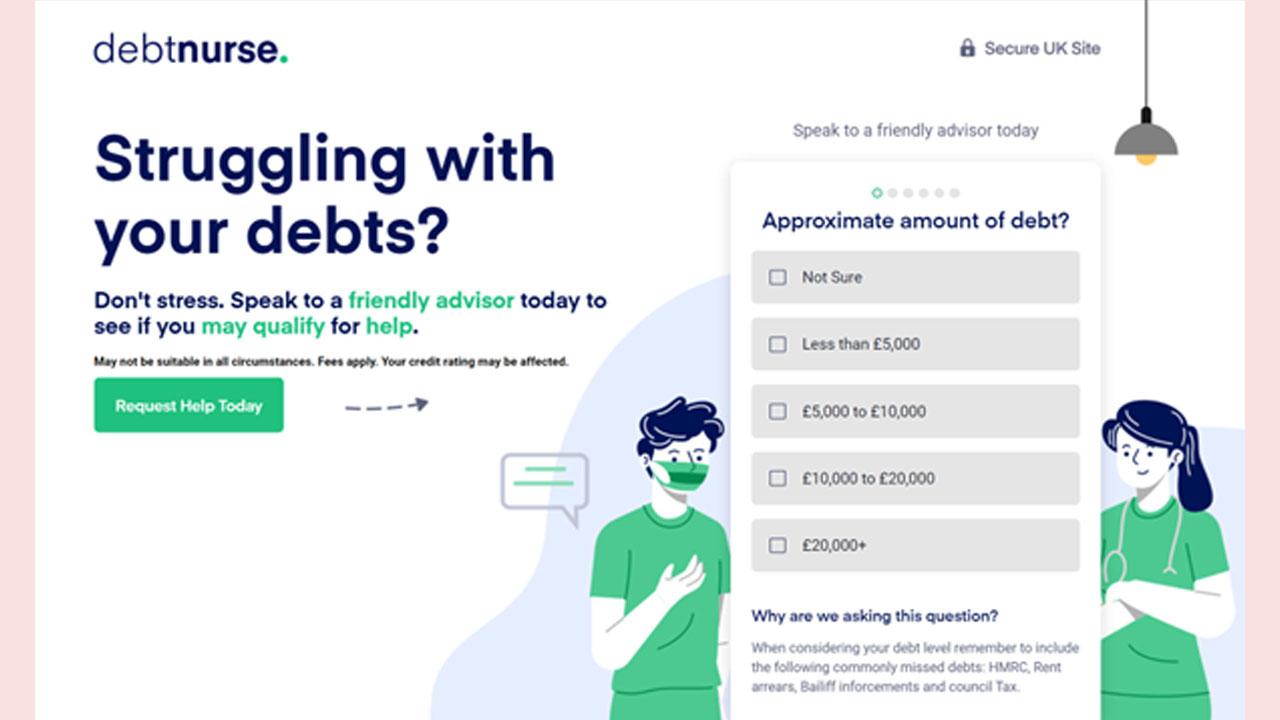

Debt Nurse: Leading Platform for Gathering IVA Debt Help and Guidance

Debt Nurse is one of the best platforms for accessing IVA debt help and guidance from authorised debt solution providers. Although they don’t offer debt advice, they work with IVA debt help providers regulated by the FCA and can connect you to them through a swift online process. Simply complete the online form and consent to referral to get immediate and impartial help and guidance on your debts.

Highlights of Gathering Expert IVA Debt Help

- Help from FCA-regulated providers

- Swift online process

- Immediate feedback

- Impartial advice

Pros of IVA Debt Help via Debt Nurse

- Prevent creditor harassment

- Avoid additional fees from charges and interest

- Reduce your debt through easy payments

Cons of IVA Help via Debt Nurse

- Objections from some creditors

Viva Debt Help: Recommended Platform for Consulting with IVA Debt Management Advisors

Help My Debts Pro is a top option for connecting with debt IVA advisors in the UK within minutes. The user-friendly platform has a stellar reputation for connecting overindebted UK residents with legitimate third-party IVA debt advisors. You only need to fill in a no-obligation form and consent to share your details with a suitable advisor who will offer immediate feedback to help you decide with zero pressure.

Highlights of Connecting with Debt IVA Advisors

- User-friendly process

- Excellent reputation

- Immediate feedback

- Zero pressure

Pros of Connecting with Debt IVA Advisors

- Asset protection

- You get to understand your options

- Stress-relief from debtors

Cons of Connecting with Debt IVA Advisors

- Only suitable for unsecured debts

123 Debt Fix: Good Starting Point for People Interested in an IVA Debt Write Off

123 Debt Fix is a good starting point if you're unsure how to become debt-free. Although the platform doesn’t offer debt advice, you can rely on it to access FCA-approved debt solutions providers who can help with an IVA debt write-off. The entire process is private and confidential, and you don’t have to go through red tape to get help reducing or eliminating unaffordable debt.

Highlights of IVA Debt Write Off

- Reliable services

- FCA-approved professionals

- Privacy and confidentiality guaranteed

- Zero red tape

Pros of an IVA Debt Write Off

- A clear roadmap to becoming debt-free

- Reduce or eliminate debt

- Stop charges and interest

Cons of an IVA Debt Write Off

- It may not help with all debts

What is an IVA Debt Write Off?

An IVA debt write-off is when leftover debt balances are discharged after completing the IVA term. The IVA is a legally binding, affordable way to repay all or part of your debts through easy repayments over an agreed period of five or six years. It involves an agreement between you and the creditors where charges and interest are frozen to prevent the debt from increasing and make it easier to afford monthly payments.

A court usually approves IVA debt write-offs, and they’re usually set up and managed by an insolvency practitioner (IP). The IP can help you work out a suitable repayment plan based on your circumstances, including monthly payments, a lump sum, or a combination of both. Being truthful about your financial situation is vital so the practitioner can determine how much you can realistically repay your creditors. Once you work out a repayment plan, the IP will help you propose it to the courts and your creditors, and the IVA will begin once 75% of the creditors agree.

Debt Management Plan vs IVA and Other Alternatives

You can choose from different debt relief options depending on your situation. These include:

Debt Management Plan

Unlike IVAs, a debt management plan (DMP) is an informal agreement with the people you owe money to make affordable repayments and reduce the pressure of high monthly payments. DMPs usually cover unsecured debts and are arranged by third-party debt solutions advisors.

They examine your situation, budget, and finances to determine how much you can afford monthly after deducting priority payments and living expenses. Once you make the payment, the solutions provider divides it among creditors to cover the debts included in the plan.

Debt Relief Order

A debt relief order (DRO) is a solution that can help you deal with debts you cannot repay. It can help you make a fresh start by freezing payments and interest for debts listed on the DRO. It can last for 12 months, and after this period, you don’t have to repay the debts, provided your situation doesn’t change. You’ll need an approved debt advisor to apply for a DRO, and it’s usually a suitable solution if you have limited income and assets and owe less than £30,000 in total.

Debt Consolidation

Debt consolidation involves taking out a new loan to pay off multiple debts, so you’re only left with one loan to repay. It allows you to combine multiple debts into a single loan, allowing you to get more favourable terms like lower rates and affordable monthly repayments. You can consolidate debt by taking out a large personal or home equity loan to pay off smaller debts. This helps simplify your financial life by leaving you with fewer monthly payments and ensuring you only deal with one lender instead of multiple.

What is IVA Debt: IVA Debt Meaning

Some factors and features you can expect with IVA debt help include:

Professional Advice from FCA Approved Debt Solution Advisors

You can expect professional advice from debt solution advisors who have been approved and regulated by the FCA. They can assess your situation and debts and help you select the best action to become debt-free. You can trust debt solutions and advice from experts authorised by the FCA since they must adhere to set regulations and guidelines. Such rules require them to be honest about all the information and upfront regarding the fees involved.

No Obligation Debt Advice

The above platforms only connect you to impartial advisors who don’t pressure you into accepting a particular debt solution. They’ll only help you understand your options so you can make an informed decision.

Write Off Debts Over 5000

It’s usually recommended to include and write off debts over 5,000 using an IVA because of the charges involved, which can consist of set-up fees and handling fees every time you make a payment.

What’s an IVA Debt Plan? What Debts Can Write Off with an IVA

IVA debt plans are legal agreements with creditors that allow you to repay your debts affordably for an agreed period. Remaining debts are usually written off after completing the IVA. Debts you can write off include family or friend debts, overdrafts, personal unsecured loans, store cards, credit cards, and payday loans.

Can I Change from IVA to Debt Plan, and What Costs Are Involved?

Yes. You can change from an IVA to a debt management plan if you change your mind or your financial situation changes. Costs can include increased payments or the possibility of creditors seizing your assets since the DMP isn’t legally binding.

How to Apply for IVA or Debt Management Plan

You can apply for an IVA in the UK through Debt Nurse using the following steps:

Step 1: Complete the IVA Debt Consolidation Application Form

You only need a few minutes to fill out the online no-obligation form with information on your debts. It’s easy to follow, secure and confidential.

Step 2: Wait for a Call from a Qualified FCA-Approved Debt Advisor

Debt Nurse will connect you with a qualified FCA-approved debt advisor who will contact you to discuss your situation and guide you through the process.

Step 3: Find a Solution to Reduce Your Debts

The advisor will provide information and advice on all the options available to you. They’ll help you choose a suitable solution based on your income, budget, and outgoings. You can allow the advisor to set it up, but it’s not an obligation, so there’s no pressure to proceed.

FAQs

Will An IVA Debt Management Plan Impact My Borrowing?

Yes. The IVA will be publicly shown on your credit reference file for six years and three months after the IVA ends. Lenders will see the IVA when performing credit checks, making borrowing challenging.

How Does a Debt Relief Order vs IVA Differ?

A DRO usually lasts for around one year, while an IVA can last for five years or longer. DROs also don’t feature fees, while IVAs include various costs and expenses, including handling fees, set-up fees, and professional costs for arranging the IVA and meeting with creditors.

How Much Debt Can I Include in an IVA Debt Relief?

Although there’s no minimum or maximum limit on the amount of debt, many providers recommend only including debts of at least £5000. Some providers also require you to have debts from at least two creditors to qualify for an IVA. You can consider other debt solutions if you owe less than £5000.

What Happens If I Default on IVA Debt Plan Payments?

The insolvency practitioner will send you a notice of breach when you miss payments. The notice will require you to explain why you defaulted within three months. The IP may not take further action if you provide a reasonable explanation, but if you don’t, they can take court action and make you bankrupt, end it, or change the IVA terms.

Can Creditors Included in the Individual Voluntary Agreement Contact Me?

Creditors included in the IVA should not contact you. They’re legally bound by the agreement whether they agreed to it or not, and you should inform the IP immediately if they’re harassing you.

Conclusion

IVA debt advice can help you find a suitable solution if you owe substantial unsecured debts to multiple creditors and are struggling to afford repayments. Debt Nurse offers fast and easy access to some of the best IVA debt help advisors authorised by the FCA to provide debt guidance and solutions.

Disclaimer: Mid-Day holds no responsibility or liability for any direct, indirect, implied, punitive, special, incidental, or consequential damages resulting directly or indirectly from the use of this content. It is advisable to seek guidance from an expert advisor or health professional as the information on the site is not a substitute for professional medical advice, diagnosis, or treatment. The information provided should not be used for diagnosing or treating a health problem or disease, and individuals seeking personal medical advice should consult with a licensed physician. The views and opinions expressed in this sponsored article are those of the sponsor/author/agency and do not represent the stance or views of Mid-Day. Any purchases made from the branded segment are at your own discretion and risk.

Subscribe today by clicking the link and stay updated with the latest news!" Click here!

Subscribe today by clicking the link and stay updated with the latest news!" Click here!